In my October 23,2021 Article, I wrote about the Single Family Rental Market: 2024

Here are the key takeaways from that article:

Home Values – Year over year change in home values as per John Burns Real Estate Consulting were projected to be:

- 2022 = 4%

- 2023 = 3%

- 2024 = 0%

Rents

- Over the last 35 years, there were only 3 years where rents declined

- Rental rates NEVER declined 2 years in a row (or twice within any 5 year period for that matter)

- The highest 1 year decline was only 2.3%

- Historical average yearly rent growth for new leases is 3.4%

- Rents were projected to grow 4.9% in 2022, 4.1% in 2023 and 3.1% in 2024

To conclude the article I pointed out that I would be watching the following 4 things leading up to 2024::

- Will housing supply not only catch up but ultimately overtake demand and if so when?

- With unprecedented financial stimulus, will inflation run rampant and force the federal reserve to raise interest rates?

- Even though interest rate increases have not led to home price declines in the past, if rates increase, will prices decline?

- And most importantly, will we start to see consistent and greater than normal declines in rental rates?

So where are we now?

Home Values

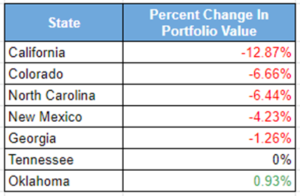

2002 is not yet finished but below is a chart showing the percent DECLINE of a clients homes since June in the various markets where they own property:

It’s important to note that this is not year over year data. These declines have happened in only 5 months.

Am I concerned?

Well, certainly one gets a better feeling when assets they own are not quickly decreasing in value, but there are 2 things to consider here.

- Home price appreciation in 2020 and 2021 was historically high. So we are coming down quickly but it’s from a very high perch.

- Most importantly, as I have written several times, as a long term buy and hold real estate investor, I don’t care all that much about home values in the short term. (Glad I’m not a “buy low, sell high” stock investor with the Nasdaq, as of this writing, down 31% for the year)

Rents

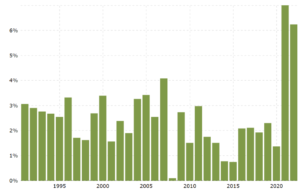

By far, I’m most interested in rents. In my article entitled, My Favorite Economic Chart, I shared that the historical rental trend line is a thing of beauty.

Here is the updated chart since 1950 that adds in the last 17 months of data since the article was published

The chart gradually goes up and to the right with very little volatility. Rent growth has historically been highly predictable. Love that. Predictability is the foundation of durable businesses and this is one of the main reasons I have a great deal of confidence in the long term buy and hold model.

The last 2 years have been some of the most anomalous, with rents rising much faster than normal. I have personally experienced this as well, as I have seen market rents for my units bump up quickly.

So while home values in some markets are coming down, rents are remaining relatively stable

So What’s Driving The Market?

As per above, one of the 4 questions I posed last October was: “With unprecedented financial stimulus, will inflation run rampant and force the federal reserve to raise interest rates?”

The answer is an unequivocal and resounding yes.

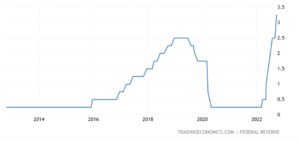

As per below, inflation, as measured by the Consumer Price Index (CPI), has spiked precipitously and is at a 30 year high.

… and what has the Federal Reserve done……

They have aggressively raised the benchmark Federal Funds Rate at a historic pace.

In addition, they have started “quantitative tightening”. Without getting into all the details, QT is a bond related program which also aims to decrease the availability of money by, in essence, increasing the risk adjusted cost of borrowing it.

The most basic definition of inflation is that prices rise because too much money is chasing after too few goods. By increasing the cost of money and making access to credit more restrictive (higher rates), the theory is that demand will decrease and get closer aligned with supply which will decrease inflation. . The Federal Reserve typically targets 2%.as the healthy rate of inflation.

The benchmark 30 year fixed rate mortgage was at an average of 3.2% in early January of this year. As a result of the Fed’s actions, at the end of September it was more than double at 6.7%

Home Values In Relation To Interest Rates

Another one of the 4 questions I posed last October was, “Even though interest rate increases have not led to price declines in the past, if rates increase, will prices decline?”

We are strongly trending towards a full body yes.

Somewhat counter-intuitively whenever interest rates have gone up in the past, housing prices have also risen. The reason is because the Fed has raised rates during periods of strong economic growth, low unemployment and strong wage growth. These factors are all strongly correlated with the demand to own homes and the ability for people to pay for them..

What’s different this time around? A few things:

- While unemployment is low and wages have been growing, economic growth (as measured by GDP) has been stagnant.

- As a result of the pandemic and its associated stimulus program, the Fed increased the supply of money by 40% from March of 2020 to March of 2022.

- The last 2 years saw unprecedented home price appreciation. Appreciation that even outpaced the increases leading up to the Great Recession in 2008.

- As more and more people feel the pain of persistent inflation, consumer confidence has plummeted to record lows.

The Future Of Rents

The most important question I posed last October was: “Will we start to see consistent and greater than normal declines in rental rates?”

Will my favorite economic chart start to turn south and disappoint?

Declining rents are on par with unexpected exorbitant maintenance costs as the biggest fear of buy and hold investors.

The bearish scenario for rents is if inflation continues to persist without reasonable wage growth and if unemployment spikes.

In these scenarios, renters would continue to spend a growing percentage of their income on food, gas and other necessities and therefore will have less to spend on rent.

Additionally, higher inflation and higher unemployment will lead to a decline in new household formation which is a key driver in keeping rents stable. Those currently living with others (family members or roommates) are more apt to stay put and those currently not living with family or roommates may look to cohabitate in order to reduce their housing costs.

The other side of the rent stability spectrum is rooted in the fact that as interest rates have rapidly risen, the number of people that both can and want to buy a home has decreased. When rates were at 3.2%, the principal and interest payment on a $300,000 loan was. $1,297 at 6.7% the payment was $1,936, a difference of $639 per month.

But of course, they still need a place to live.

With work from home here to stay and the large cohort of millennials starting families (wanting yards and space for their pets) the demand for single family rentals should stay strong. This strong rental demand should keep rents within the bounds of historical trends.

Even if rents were to decline over the next few years, they would be declining from a very high perch, similar to home values.

Is There Opportunity For Buy & Hold Investors?

The best acquisition opportunities come when there are highly motivated sellers. I started to scale my portfolio in 2009/2010 when banks, who are not in the business of owning and operating homes, had a lot of them on their balance sheet (foreclosures) and needed to get rid of them. They were highly motivated sellers.

So will there be a wave of motivated sellers?

I have written several pieces explaining the power of the 30 year fixed rate mortgage. Example: 3 Ways Investors Can Have Their Cake & Eat It Too

Not all investors/owner occupants who bought recently at high prices used long term fixed interest rate loans. This is because shorter term variable rate loans can have much lower payments at the outset. These folks assumed some combination of the following for when the term of their loan comes up:

- Interest rates would be relatively the same and the property could be refinanced with similar terms.

- The property appreciated significantly (and certainly not declined in value)

- Rents would have gone up significantly or at least an amount that offsets any interest rate increases

Here’s a basic example.

For simple math, let’s say that in 2021 an investor acquired an asset with a variable rate mortgage that resets in 3 years. Income from rent for the property is $3,500 and the monthly loan payment is $2,500 for a difference of +$1,000.

In 2024, not only may the value of the property be less, but their loan will reset to current market rates. Let’s say their loan payment then becomes $4,500. In this case the difference is -$1,000.

The owner will have the choice of either losing $1,000 per month or quickly liquidating the property (motivated seller) to stop the recurring loss.

I think these type of opportunities will be coming over the next few years when investors who chose short term variable rate loans to acquire properties will be highly motivated to sell them

Investors who have cash reserves and are willing to act during uncertain/volatile economic times, will be in a very strong position to pick up these assets at lower prices and cash flow them.

Another group of sellers that I can see become highly motivated over the next few years are small builders. Unlike owner occupants or non distressed investors, Builders, based on their business model, have to sell their product.

Builders typically use the proceeds from their sales to pay off the short term money they borrowed to build the homes. If sales and prices decline, at the same time their loans are due, they are put in the un- enviable position of having to refinance at higher rates with uncertainty of how much they will actually be able to sell their homes for.

A group of these builders will opt to sell quickly (motivated) and at prices favorable to buyers vs risking cash bleed over an uncertain time period.

Summary:

Inflation is very high and to combat this, the Federal Reserve Bank Of The United States is raising interest rates.

Home values are beginning to decline in many markets despite history telling us that home value declines are not typical when interest rates rise. This is in large part because of the massive pandemic related economic stimulus and unprecedented home price appreciation leading up to the interest rate increase. .

Over the last 2 years, rents, which typically increase very steadily over time, have increased at historically high rates.

Over the next few years, investors/owners and under capitalized builders that recently acquired or built homes with short term variable rate debt and under the wrong set of assumptions may become highly motivated sellers. This will present an opportunity for investors with a long term time horizon that have cash reserves and believe that rent stability will persist.