Historically,what’s happening with home PRICES tends to get the most press and attention from the collective psyche of shelter conscious Americans.

While prices are a major factor that drive housing behavior, there is a lot more to the story.

More recently, and justifiably so, what’s happening with INTEREST RATES, has garnered more of the headlines. The 30-Year Fixed Rate Mortgage has more than doubled over a very short period of time and this precipitous rise has had a meaningful impact on not only demand for housing but also, less intuitively, supply (more on this later).

Most American’s decision to purchase a home, or not, comes down to if they can make the monthly payment. The 3rd major factor then, is how much Americans are earning or their WAGES.

PRICE, INTEREST RATES, WAGES

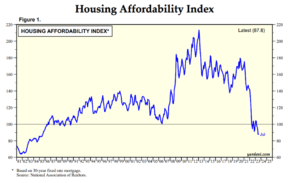

The chart below going back to 1981 shows the Affordability Index which accounts for these 3 factors.

Housing affordability has plummeted and it has never been less affordable in most of this readership’s adult lifetime.

If No One Can Afford A House, Why Haven’t Prices Crashed?

If more and more people are unable to afford a house, it’s logical to assume that prices would need to drop significantly. But they haven’t and many experts predict they will not in the foreseeable future. Why?

Supply. 62% of existing homeowners have a mortgage rate below 4%. 23.5% are below 3% (I’m in this bucket for my primary residence).

Selling a home with a 3% mortgage rate to move into a similar home that will cost more and come with a 7%+ rate makes absolutely no financial sense.

Unless homeowners HAVE TO sell for some reason, they will stay put. This “Lock In” effect has caused the sale of existing homes to plummet simply because there are no homes to buy.

I know that if for some reason I needed to move, I would not sell my home and give up my 2.65% mortgage. I would keep the loan and the home as a rental.

At the same time, while rising interest rates have destroyed some marginal demand, overall, demand has not gone down enough relative to supply to cause prices to crash.

For more about demand, see “The Secret Is Out: Will The Housing Market Ever Be The Same”

In addition, all cash buyers are not concerned with interest rates. With this demand dynamic, houses that do come on the market in most geographic markets still get high interest from multiple buyers which keeps prices buoyant.

Buying Vs Renting

The graphic below gives further insight into the lack of affordability. The dramatic and historic rise in the cost to buy a home as measured by monthly payment is astonishing. The gap between how much it costs to buy vs rent has never been greater.

So What Can We Do

The good news for existing rental property owners is that rental demand for single family residences will stay high.

The challenge is for those that want to grow their portfolio or are just getting started.

Given the The Power Of The Buy & Hold Model, my belief in acquiring and owning rental properties for the long term has never waivered over the last 2 decades.

However in this current environment of high prices, high interest rates, high homeowner equity, low supply and high latent demand, new investors seeking cash flow from day 1 need to understand that finding good deals will be very hard. It will require more time and effort relative to recent history. Additionally, it will take longer to meaningfully reap all 5 of the benefits.

With existing home supply expected to remain very low, working directly with builders could have some advantages. Unlike locked-in existing homeowners, builders HAVE TO sell their homes and depending on how aggressively they have built in a given market they may become motivated. Builders also have the ability to buy down interest rates for buyers.

Those that can save cash to build sizable down payments or avoid having to get a loan all together will be advantaged.